COMMERCIAL REAL ESTATE (CRE)

Commercial Real Estate is one of the most resilient and globally recognised investment asset classes. From income-producing hotels and logistics platforms to healthcare facilities, retail parks, and mixed-use developments, commercial property plays a central role in economic growth and long-term wealth creation.

In today’s market, successful CRE transactions require far more than traditional brokerage. They demand disciplined underwriting, strategic capital structuring, and institutional execution.

At Esteema Capital Partners, we operate as a discreet strategic capital advisor across the United Kingdom and selected global prime markets, supporting sponsors, developers, family offices, and institutional investors in structuring and executing complex real estate transactions.

Our expertise combines:

• Strategic capital structuring

• Asset repositioning and value-enhancement strategy

• End-to-end transaction management and execution oversight

Our Focus

Delivering certainty, discretion, and efficient execution across mid-to-large commercial real estate transactions.

Whether acquisition, development, refinancing, recapitalisation, or strategic exit, we align capital, structure, and strategy to optimise returns while managing downside risk.

Sectors We Support

We structure capital solutions across major commercial real estate sectors, including:

Hospitality & Living Platforms

Branded and independent hotels, serviced living, Build-to-Rent (BTR), PBSA, and mixed-use developments.

Healthcare & Operational Real Estate

Care homes, healthcare platforms, forward-funded developments, and income-producing operating assets.

Retail & Regeneration

Retail parks, high street investments, mixed-use regeneration, and repositioning strategies.

Industrial & Logistics

Last-mile logistics, light industrial, urban warehousing, and distribution platforms.

Office & Alternative Assets

Prime and secondary offices, life sciences, data centres, and other institutional real estate sectors.

Locations We Support

• United Kingdom & Global Prime Markets

Supporting commercial real estate transactions across the UK and selected prime international markets, working with developers, sponsors, investors, and institutional counterparties.

• Cross-Border & Multi-Currency Transactions

Experience in international transactions including multi-currency financing, overseas investor participation, SPV structuring, and coordinated legal execution across jurisdictions.

• Strategic Transaction Execution

Advising on acquisitions, investments, refinancing, and portfolio transactions, ensuring efficient execution across complex global real estate markets.

WE SUPPORT: Strategic Capital Architecture Across the Full Real Estate Lifecycle

At Esteema Capital Partners, our focus is not brokerage — it is capital structuring.

We design, align, and execute institutional-grade capital solutions across acquisitions, developments, recapitalisations, and long-term asset growth strategies.

1. Capital Structuring & Investment Architecture

-

Senior debt, stretch senior, mezzanine & preferred equity structuring

-

Acquisition, development & investment capital stack optimisation

-

Joint venture structuring and sponsor–investor alignment

2. Multi-Currency & Cross-Border Structuring

-

GBP, EUR, USD and selected GCC-linked capital arrangements

-

FX-aligned debt structuring and currency risk mitigation

-

Cross-border SPV and holding structures for international investors

3. International & Offshore Investment Structuring

-

UK inbound investment structuring for offshore investors

-

Tax-efficient SPV and holding company frameworks

-

Alignment between UK regulatory requirements and international capital

4. Recapitalisation & Capital Re-Engineering

-

Balance sheet optimisation and equity release strategies

-

Debt restructuring and re-gearing advisory

-

Portfolio recapitalisation and structured exits

5. Long-Term Strategic Capital Advisory

-

Ongoing capital planning and growth strategy alignment

-

Institutional reporting and governance support

-

Future refinance, expansion and exit roadmap planning

Esteema ‘Capital & Investments’ Expertise Delivers ‘Diversified Global Capital’

Complete Capital Stack & Syndicated Solutions

-

Senior, stretch senior, mezzanine, preferred equity and JV capital structuring

-

Club deals and syndicated funding for large, complex and multi-jurisdictional transactions

-

Multi-currency solutions with optimised leverage and institutional underwriting standards

Multi-Family Private Office Lifecycle Capital Advisory

-

Acquisition, development and repositioning capital structuring

-

Stabilisation, recapitalisation and strategic refinance planning

-

Exit alignment focused on IRR optimisation, liquidity timing and downside protection

Special Situations & Structured Capital

-

Institutional underwriting with disciplined risk governance frameworks

-

Structured debt, hybrid capital and bespoke equity solutions

-

High-certainty execution for time-sensitive or complex capital events

Multi-Sector Capital Expertise

(Real Estate | Hospitality | Healthcare | Commercial Assets | Special Situations Finance)

-

UK and cross-border SPV structuring expertise

-

Capital alignment across tax, regulatory and investor frameworks

-

Deep sector insight supported by institutional capital relationships

Cross-Border & Offshore Capital Alignment

-

Inbound UK investment structuring for international investors

-

GCC, European and global family office capital access

-

Currency, regulatory and governance alignment for international transactions

Commercial real estate financing requires specialist expertise — particularly where bespoke structuring is essential and conventional lending approaches fall short.

At Esteema Capital Partners, we combine real estate, corporate finance, and legal structuring expertise to design tailored capital solutions for complex transactions.

Esteema CRE Specialist Finance | Other Traditional Finance | |

|---|---|---|

| ✓ Any Type | Retails, offices, industrial, shopping centre Student Accommodation, Hotel & Leisure etc | No |

| ✓ Any Purpose | Purchase, Refinance, Re-Structure | No |

| ✓ Any Borrower | UK & International | No |

| ✓ ANY SPV | UK or Offshore | No |

| ✓ Any Location | UK or Global Prime Location | No |

| ✓ Multi-Currency & Cross Border Funding | Yes | No |

| ✓ Loan Size | No Upper Limit | Very Restricted |

| Leverage | Up to 80% | Very Restricted |

| Interest Rate | from 5.5% + | From 5%+ onward |

| Any Special Reasons | ✓ Non-Recourse ✓ No maximum age ✓ Any Legal Settlements | No |

Esteema CRE Special Pricing

Small CRE Loan

Less than £5M

Rates from:

5.5% PA

Up-To

75% Loan to Value

Large CRE Loan

More than £5M

Rates from:

5.5% PA

Up-To

75% of Loan to Value

Portfolio / Mixed

(No upper Limit)

Rates from:

5.5% PA

Up-To

75% Loan to Value

Key Factor Affecting the Commercial Real Estate Financing

Borrower & Sponsor Profile

✓ Sponsor track record and sector experience

✓ Personal and corporate financial strength

✓ Income sustainability and cash flow profile

✓ SPV structure, governance and jurisdiction

Asset & Collateral Profile

✓ Asset class and operational characteristics

✓ Market demand, rental resilience and liquidity

✓ Location quality and tenant covenant strength

✓ Lease structure, WAULT and covenant terms

Debt & Loan Service Metrics

✓ Loan-to-Value (LTV) and leverage structure

✓ Current and stabilised rental income profile

✓ Gross vs Net income coverage ratios

✓ Financial covenants and downside protection

Commercial Real Estate Capital Market Guide

Capital Stack Guide

COMMERCIAL REAL ESTATE CAPITAL STACK GUIDE

Institutional Structuring | Risk Framework | Capital Strategy

1. What is Commercial Real Estate Capital?

Commercial real estate (CRE) capital refers to the structured financing and equity solutions used to acquire, develop, reposition, refinance, or recapitalise income-producing commercial property.

Unlike residential lending, CRE capital is underwritten primarily on:

-

Asset cash flow performance

-

Sponsor track record

-

Risk-adjusted return profile

-

Capital structure resilience

It combines debt, equity, and hybrid instruments aligned to institutional underwriting standards.

2. Types of Capital in CRE Transactions

Senior Debt

Traditional bank or institutional lending secured against the asset, typically structured around LTV and income coverage metrics.

Stretch Senior & Whole Loan

Higher leverage solutions with blended pricing and simplified capital stack execution.

Mezzanine Finance

Subordinated capital sitting behind senior debt, enhancing leverage while preserving sponsor equity.

Preferred Equity

Structured equity with priority return, often used to bridge funding gaps without additional debt burden.

Joint Venture (JV) Equity

Institutional or private capital partnering with sponsors for large or complex transactions.

| Loan Type | Purpose |

|---|---|

| Senior commercial mortgage | stabilized assets |

| Bridge finance | acquisition / transition |

| Development finance | construction |

| Mezzanine finance | leverage enhancement |

| Structured debt | complex transactions |

3. Key Capital Metrics

Institutional capital decisions are driven by:

-

Loan-to-Value (LTV)

-

Debt Service Coverage Ratio (DSCR)

-

Yield on Cost (Development)

-

Stabilised NOI

-

Exit Yield & IRR projections

-

Covenant structure & downside protection

These metrics determine leverage capacity, pricing, and risk tolerance.

4. Capital by Transaction Type

Acquisition Capital

Structured to optimise leverage while maintaining covenant flexibility.

Development Finance

Phased drawdowns, cost monitoring, and forward-funding strategies aligned to exit assumptions.

Repositioning & Value-Add

Transitional capital, bridging finance, and stabilisation funding.

Refinancing & Recapitalisation

Equity release, debt restructuring, and balance sheet optimisation.

5. Cross-Border & Multi-Currency Structuring

For international investors, CRE capital may involve:

-

GBP, EUR, USD structured debt

-

Offshore SPVs and holding companies

-

Tax-efficient structures aligned with UK regulations

-

Currency risk mitigation strategies

Cross-border structuring requires coordination between legal, tax, and capital providers.

6. Why Specialist Capital Advisory Matters

Commercial real estate capital is complex — particularly where:

-

Traditional lending frameworks fall short

-

Transactions involve multiple jurisdictions

-

Sponsors require higher leverage

-

Assets are operational (hospitality, healthcare)

-

Time-sensitive execution is critical

Institutional-grade structuring significantly improves funding certainty and execution speed.

How Esteema Supports CRE Capital

At Esteema Capital Partners, we design and align full capital stacks across acquisition, development, recapitalisation, and strategic exits.

We combine:

-

Institutional underwriting discipline

-

Structured debt and equity architecture

-

Cross-border SPV expertise

-

Multi-family office capital access

-

High-certainty execution capability

Delivering structured, globally aligned capital solutions across UK and selected international markets.

CRE Capital Structuring Process & Key Documentation

COMMERCIAL REAL ESTATE CAPITAL

Process & Key Documentation Framework

Our Capital Structuring Process

Commercial real estate capital requires disciplined execution from initial review through completion. Our process is designed to maximise funding certainty while protecting sponsor and investor interests.

1. Strategic Review & Initial Assessment

-

Sponsor profile, track record and financial strength review

-

Asset underwriting (income, tenancy, market position, liquidity)

-

Capital requirement analysis (acquisition, development, refinance, recapitalisation)

-

Target leverage, pricing expectations and exit strategy alignment

Outcome: Clear capital strategy and structuring roadmap.

2. Capital Stack Design & Structuring

-

Senior debt, stretch senior, mezzanine or preferred equity optimisation

-

Leverage modelling and covenant sensitivity analysis

-

Multi-currency and cross-border structuring (if applicable)

-

SPV and holding structure alignment

Outcome: Institutional-grade capital architecture aligned to risk profile.

3. Credit Packaging & Lender Engagement

-

Preparation of funding memorandum / credit paper

-

Financial model validation and stress testing

-

Targeted engagement with aligned lenders, private credit funds or equity partners

-

Term sheet negotiation and structure optimisation

Outcome: Competitive, aligned capital terms.

4. Due Diligence & Execution

-

Valuation, legal, technical and commercial DD coordination

-

Facility documentation review and covenant negotiation

-

Intercreditor agreements (where layered capital is involved)

-

Drawdown structuring and completion management

Outcome: High-certainty closing with structured risk mitigation.

5. Post-Completion Capital Oversight

-

Ongoing covenant monitoring support

-

Refinance and recapitalisation planning

-

Exit strategy alignment (sale, IPO, portfolio restructuring)

-

Long-term capital advisory

Outcome: Lifecycle capital alignment beyond initial transaction.

Key Documentation in CRE Capital Transactions

Institutional capital providers typically require:

Sponsor & Corporate Documents

-

Company incorporation documents & SPV structure

-

Director and shareholder information

-

Track record & asset portfolio summary

-

Personal / corporate financial statements

Financial & Investment Documents

-

3–5 year financial model

-

Cash flow projections & sensitivity analysis

-

Capital stack breakdown

-

IRR & exit assumptions

Asset Documentation

-

Independent valuation report

-

Tenancy schedule & lease summary

-

WAULT analysis

-

Planning & development approvals (if applicable)

Legal & Risk Documentation

-

Title documents

-

Existing loan agreements (if refinancing)

-

Environmental & technical reports

-

Corporate guarantees (where applicable)

Execution Philosophy

Our role is not merely to introduce capital — but to structure, align and execute with institutional discipline.

We ensure capital solutions are:

-

Risk-adjusted

-

Covenant-aligned

-

Tax & regulatory efficient

-

Designed for long-term flexibility

Key Reason of Loan Rejection | CRE Underwriting Criteria

Key Reason of Loan Rejection | CRE Underwriting Criteria

Commercial mortgage underwriting is a structured process through which lenders assess the risk, viability, and repayment capacity of a transaction before approving finance.

Institutional lenders evaluate several key parameters to ensure that the asset, borrower, and capital structure meet their investment and risk requirements.

At Esteema Capital Partners, we help sponsors and investors structure transactions to meet institutional underwriting standards, improving approval probability and execution speed.

1. Asset Quality & Location

Lenders first assess the quality and market position of the property.

Key factors include:

-

Prime vs secondary location

-

Asset type (hotel, office, logistics, healthcare, retail, mixed-use)

-

Market demand and supply dynamics

-

Local economic indicators

-

Future redevelopment or repositioning potential

For example, a prime London hotel asset will generally receive stronger underwriting support than a secondary regional asset.

2. Loan-to-Value (LTV)

Loan-to-Value measures the relationship between the loan amount and the asset valuation.

Typical market ranges:

| Asset Type | Typical LTV |

|---|---|

| Stabilised prime assets | 60% – 70% |

| Value-add assets | 55% – 65% |

| Development finance | 50% – 65% (LTGDV basis) |

| Special situations | Case-by-case |

Lower LTV typically results in better pricing and stronger lender appetite.

3. Debt Service Coverage Ratio (DSCR)

DSCR measures the borrower’s ability to repay debt from property income.

Formula

DSCR = Net Operating Income ÷ Annual Debt Service

Typical lender requirements:

-

Minimum 1.20x – 1.35x for stabilised assets

-

Higher coverage for riskier assets

A higher DSCR indicates stronger income protection for lenders.

4. Net Operating Income (NOI)

The income generation capability of the asset is critical.

Lenders analyse:

-

Historical operating performance

-

Stabilised income projections

-

Tenant covenant strength

-

Lease structure and length

-

Vacancy levels

For hospitality assets, lenders evaluate:

-

EBITDA performance

-

Brand strength

-

Operator covenant

5. Sponsor / Borrower Strength

Institutional lenders heavily assess the track record and financial strength of the sponsor.

Evaluation includes:

-

Previous transaction experience

-

Asset management capability

-

Balance sheet strength

-

Liquidity and cash reserves

-

Reputation and governance

Experienced sponsors significantly improve underwriting outcomes.

6. Exit Strategy

Lenders must clearly understand how the loan will be repaid.

Typical exit strategies include:

-

Asset refinance

-

Asset sale

-

Stabilisation and long-term refinancing

-

Portfolio recapitalisation

A credible exit strategy is a core underwriting requirement.

7. Tenant & Lease Analysis

For income-producing assets, lenders evaluate tenant strength and lease security.

Key factors:

-

Tenant credit rating

-

WAULT (Weighted Average Unexpired Lease Term)

-

Rent review structures

-

Break clauses

-

Tenant diversification

Strong tenants significantly reduce lender risk.

8. Valuation & Independent Reports

Lenders rely on independent professional reports.

Typical required reports include:

-

RICS Valuation Report

-

Building Survey

-

Environmental Assessment

-

Market Study

-

Cash Flow Analysis

For hotels or operating assets:

-

Trading performance review

-

Operator agreement analysis

9. Legal & Regulatory Due Diligence

Lenders perform full legal checks before issuing funding.

Typical legal reviews include:

-

Title verification

-

Planning permissions

-

Lease documentation

-

Corporate structure (SPV structure)

-

Security package

10. Risk Sensitivity Analysis

Institutional underwriting includes stress testing.

Lenders evaluate scenarios such as:

-

Interest rate increases

-

Vacancy increases

-

Rental decline

-

Exit valuation reduction

The goal is to ensure the asset remains resilient under downside scenarios.

11. Planning & Regulatory Compliance

Institutional lenders carefully review whether the property has been developed, altered, and occupied in full compliance with planning permissions and building regulations.

Any discrepancy between the approved planning consent and the actual building configuration or use can significantly impact loan approval, valuation, and lender risk assessment.

Key areas reviewed during underwriting include:

Planning Permission Verification

-

Confirmation that the property has valid planning permission for its current use

-

Review of planning history, including any extensions, change-of-use approvals, or redevelopment permissions

Compliance with Approved Plans

-

Verification that the building has been constructed in accordance with the approved planning drawings

-

Confirmation that there are no unauthorised structural alterations or additional units

Building Regulations & Completion Certificates

-

Evidence of building control approvals and completion certificates

-

Compliance with fire safety, accessibility, and structural standards

Lawful Use & Tenancy Compliance

-

Confirmation that the current tenancy or commercial use aligns with the permitted planning use class

-

Verification that the property is not being used for an unauthorised purpose

Planning Conditions & Restrictions

-

Review of any planning conditions attached to the consent

-

Assessment of restrictions such as operating hours, parking obligations, or community requirements

Where planning irregularities exist, lenders may require retrospective planning approval, indemnity insurance, or legal remediation before proceeding with financing.

Typical Commercial Mortgage Underwriting Timeline

| Stage | Timeline |

|---|---|

| Initial review | 3–5 days |

| Indicative terms issued | 1 week |

| Due diligence | 2–4 weeks |

| Credit approval | 1–2 weeks |

| Legal completion | 2–3 weeks |

Typical execution time: 4–8 weeks, depending on transaction complexity.

How Esteema Supports the Underwriting Process

We support clients throughout the capital raising process by:

-

Structuring bankable capital stacks

-

Preparing institutional-grade investment memorandums

-

Coordinating valuations and due diligence reports

-

Negotiating lender terms

-

Managing the transaction through to completion

Our experience across real estate, hospitality, healthcare, and corporate transactions enables faster and more reliable capital execution.

CRE Transaction Timelines & Execution Phases

Transaction Timelines & Execution Phases

Speed without structure increases risk.

Structure without urgency delays opportunity.

Our approach balances disciplined underwriting with proactive execution — delivering certainty within commercially realistic timelines.

Commercial real estate capital transactions vary in complexity, but disciplined structuring and proactive coordination significantly improve execution speed and certainty.

Below is a typical institutional execution framework:

Phase 1 – Initial Review & Structuring (Week 1–2)

-

Sponsor and asset assessment

-

Capital requirement analysis

-

Preliminary leverage and covenant modelling

-

Structuring strategy and lender positioning

Outcome: Defined capital architecture and funding roadmap.

Phase 2 – Credit Packaging & Market Engagement (Week 2–4)

-

Preparation of funding memorandum and financial model

-

Targeted lender / capital partner engagement

-

Indicative terms review and negotiation

-

Refinement of capital stack structure

Outcome: Agreed heads of terms / term sheet.

Phase 3 – Due Diligence & Credit Approval (Week 4–8)

-

Valuation, legal and technical due diligence

-

Financial stress testing and covenant alignment

-

Credit committee approval process

-

Final documentation negotiation

Outcome: Formal facility documentation issued.

Phase 4 – Documentation & Completion (Week 8–12+)

-

Legal documentation execution

-

Intercreditor agreements (if layered capital)

-

Conditions precedent satisfaction

-

Drawdown and transaction completion

Outcome: Capital deployed and transaction closed.

Accelerated & Time-Sensitive Transactions

Where transactions are deadline-driven (auction purchases, refinancing maturity, covenant pressure, distressed situations):

-

Bridging or transitional capital structures may reduce timelines

-

Streamlined credit packaging improves approval speed

-

Pre-aligned capital relationships enhance execution certainty

Execution timing ultimately depends on asset complexity, capital layering, and documentation readiness.

Typical Timeframes (Indicative)

-

Senior Debt (stabilised asset): 6–10 weeks

-

Development Finance: 8–14 weeks

-

Bridging / Transitional Capital: 3–6 weeks

-

Syndicated / Complex Structures: 10–16+ weeks

Commercial Real Estate Capital – Frequently Asked Questions

COMMERCIAL REAL ESTATE (CRE) – FREQUENTLY ASKED QUESTIONS

1. Financial & Capital Structuring FAQs

Q1. How much leverage is typically available in commercial real estate transactions?

Leverage depends on asset quality, sponsor strength, income resilience, and market conditions. Senior debt typically ranges between 55–70% LTV, with higher leverage achievable through structured mezzanine or preferred equity solutions.

Q2. Can you structure both debt and equity within the same transaction?

Yes. We design complete capital stacks — including senior, stretch senior, mezzanine, preferred equity, and JV capital — aligned to institutional underwriting standards.

Q3. What financial metrics do lenders prioritise?

Loan-to-Value (LTV), Debt Service Coverage Ratio (DSCR), net operating income (NOI), covenant strength, sponsor liquidity, and exit yield assumptions.

Q4. Do you support development and value-add strategies?

Yes. We structure phased development funding, transitional capital, stabilisation finance, and recapitalisation strategies.

2. International Client FAQs

Q1. Can international investors acquire UK commercial real estate?

Yes. We support global investors entering the UK through structured SPV frameworks aligned with regulatory and tax requirements.

Q2. Do you work with family offices and offshore investors?

Yes. We advise international family offices, UHNW investors, and cross-border capital providers seeking UK exposure.

Q3. Is a UK SPV required?

In most cases, a UK-based SPV is established for asset holding, with ownership structured via offshore entities where appropriate.

3. Cross-Border & Multi-Currency FAQs

Q1. Can financing be arranged in multiple currencies?

Yes. We structure capital in GBP, EUR, USD, and selected GCC-linked currencies, depending on lender appetite and asset profile.

Q2. How is currency risk managed?

Through structured debt alignment, hedging instruments, financial modelling sensitivity analysis, and natural income matching where possible.

Q3. Can transactions involve multi-jurisdictional capital?

Yes. Complex mandates may involve syndicated structures or club deals combining international lenders and private credit funds.

4. Legal & Structuring FAQs

Q1. What legal structures are typically used?

UK SPVs, offshore holding companies, joint ventures, and layered ownership structures aligned to tax and governance frameworks.

Q2. Do you assist with OpCo / PropCo structuring?

Yes. Particularly within hospitality and operational real estate, to optimise financing flexibility and risk allocation.

Q3. What documentation is required by lenders?

Valuation reports, financial models, tenancy schedules, corporate documentation, legal due diligence materials, and planning approvals where applicable.

5. Time-Sensitive & Special Situation Transactions

Q1. Can you support urgent or deadline-driven transactions?

Yes. We structure accelerated capital solutions for time-sensitive acquisitions, refinancing deadlines, covenant breaches, and distressed scenarios.

Q2. How quickly can funding be arranged?

Timelines vary depending on complexity, but transitional or bridging structures can be mobilised significantly faster than traditional bank-led processes when documentation is prepared efficiently.

Q3. Do you assist where traditional lenders have declined?

Yes. We specialise in complex or structured situations where conventional lending frameworks are not suitable.

6. Ongoing Advisory & Long-Term Support

Q1. Do you provide support beyond securing finance?

Yes. We operate as long-term strategic capital advisors, supporting refinancing, recapitalisation, covenant monitoring, and exit planning.

Q2. Can you assist with portfolio-level restructuring?

Yes. We support multi-asset recapitalisation and platform-level strategic capital alignment.

Q3. Do you work on single assets or portfolios?

Both — from single-asset acquisitions to large multi-asset institutional platforms.

Commercial real estate capital is institutionally driven and often time-critical. Our role is to structure disciplined, globally aligned capital solutions that enhance execution certainty, manage risk, and support long-term value creation.

Capital Markets Terminology – Vocabulary Guide

Capital Markets Terminology – Institutional Vocabulary Guide

Commercial real estate capital transactions involve layered structures, disciplined underwriting, and institutional credit terminology. The following reference framework consolidates the key concepts used by lenders, private credit funds, and equity investors.

1. Leverage & Risk Metrics

LTV (Loan-to-Value)

Debt expressed as a percentage of asset value. A primary measure of leverage and credit risk.

LTC (Loan-to-Cost)

Debt expressed as a percentage of total project cost. Common in development and repositioning finance.

DSCR (Debt Service Coverage Ratio)

Net operating income divided by total annual debt service. Measures repayment capacity and income resilience.

ICR (Interest Coverage Ratio)

Income divided by interest payments only. Frequently used in interest-only or transitional structures.

2. Income & Valuation Metrics

NOI (Net Operating Income)

Property income after operating expenses but before financing and tax. Core to valuation and debt sizing.

Yield

Annual income expressed as a percentage of asset value. Reflects market pricing and risk profile.

Exit Yield

The assumed yield at which the asset will be sold. A key driver of valuation sensitivity and IRR modelling.

WAULT (Weighted Average Unexpired Lease Term)

Average remaining lease duration across tenants. Longer WAULT generally indicates stronger income security.

3. Return & Investment Metrics

IRR (Internal Rate of Return)

Projected annualised return over the investment lifecycle, incorporating timing of cash flows and exit value.

Equity Multiple

Total cash returned divided by total equity invested.

Cash-on-Cash Return

Annual cash income relative to equity invested.

4. Capital Structure & Funding Layers

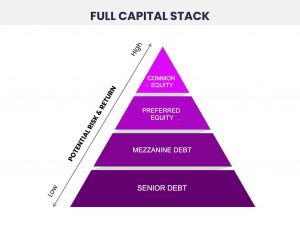

Capital Stack

The hierarchical layering of funding within a transaction:

Senior Debt → Stretch / Whole Loan → Mezzanine → Preferred Equity → Sponsor Equity.

Senior Debt

Primary secured lending with first-ranking security.

Stretch Senior / Whole Loan

Blended senior and mezzanine structure provided by a single lender to increase leverage and simplify execution.

Mezzanine Finance

Subordinated debt ranking behind senior lending but ahead of equity.

Preferred Equity

Structured equity with priority return rights ahead of ordinary equity.

Sponsor Equity

Capital contributed by the transaction sponsor, ranking last in priority but retaining upside control.

5. Legal & Structural Terminology

SPV (Special Purpose Vehicle)

A ring-fenced legal entity established to hold a specific asset or transaction.

OpCo / PropCo Structure

Separation of operating business (OpCo) from property ownership entity (PropCo), common in hospitality and healthcare transactions.

Intercreditor Agreement

Legal agreement governing rights and ranking between multiple lenders in a layered capital structure.

Covenant Package

Financial or operational conditions imposed by lenders, including LTV tests, DSCR thresholds, and cash sweep provisions.

6. Market & Execution Terms

Margin

The interest rate premium charged above a benchmark rate (e.g., SONIA or EURIBOR).

Hedging

Financial instruments (swaps, caps, collars) used to manage interest rate or currency exposure.

Club Deal / Syndication

Transaction funded by multiple lenders or investors sharing risk within a coordinated structure.

Recapitalisation

Restructuring of existing debt and equity to optimise leverage or release capital.

Refinancing

Replacing existing debt with new financing, often to improve pricing or extend maturity.

We have successfully supported numerous challenging transactions, unlike conventional channels, which could not perform.

“Unlock Capital- Transform Assets – Maximise Returns‘